The Guardian Wednesday 30 December 2015 – A glut of oil, the demise of OPEC and weakening global demand combined to make 2015 the year of crashing oil prices. The cost of crude fell to levels not seen for 11 years – and the decline may have further to go.

There have been four sharp increases in the price of oil in the past four decades – in 1973, 1979, 1990 and 2008 – and each has led to a global recession. By that measure, a lower oil price should be positive for the world economy, with lower fuel costs for consumers and businesses in those countries that import crude outweighing the losses to producing nations.

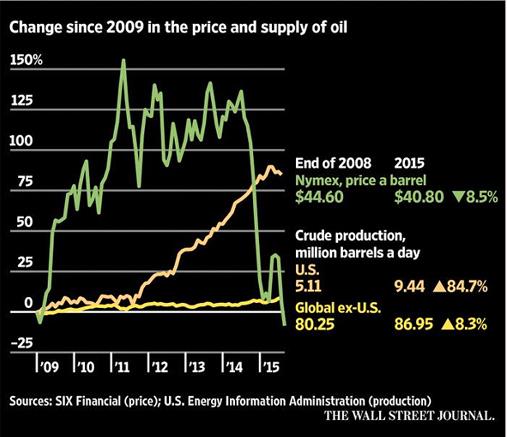

But the evidence since oil prices started falling from their peak of $115 a barrel in August 2014 has not supported that thesis – or not yet. Oil producers have certainly felt the impact of the lower prices on their growth rates, their trade figures and their public finances butthere has been no surge in consumer spending or business investment elsewhere.

Economist still reckon there will be a boost from a lower oil price particularly if it looks as if the lower cost of crude will be sustained.

For the big producer countries, this is a major headache, the ramifications of which are only starting to be felt. Oil powers base their spending plans on an assumed crude price.

Joshi says crude prices may fall by a further 35% to reach its long-term trend. That would mean an oil price closer to $25 a barrel – and fiscal crises in some of the world’s most pivotal economies.

Russia

Vladimir Putin goes into 2016 with record approval ratings but the shakiest economic outlook since he took charge. In the 15 years he has been at the helm, 2015 was the first year that real wages registered a decline, something that did not happen even during the 2008-09 financial crisis.

Oil and gas exports make up about half of the Russian budget, and the rouble ratehas been strongly linked to the price of oil.

Sanctions against Russia, particularly the ban on Russian banks seeking western credit, combined with falling oil prices in late 2014 to create a perfect storm that demolished the rouble, with the currency losing half of its value against the dollar, reviving memories of previous crashes. The currency regained some of its value by spring, but falling oil prices in autumn have caused it to fall back to lows similar to those it experienced in late 2014.

Falling oil prices were one of the principal reasons for the collapse in the Soviet economy, and some economists are warning of history repeating itself. Riding on a wave of high oil prices for most of his presidency, the Russian president did not expect such a sharp downturn. Last October, Putin said that if the price of oil fell below $80 a barrel, the world economy would crash. A range of other top Russian officials made similar statements, in effect ruling out the possibility that oil could fall below $70.

Some analysts say the rouble is still overvalued, and the current oil price should theoretically push the rouble down further. This is necessary to balance the budget: the fewer dollars Russia receives for the oil it sells, the higher the exchange rate needs to be for the budget to receive the requisite amount of roubles. For the budget to balance at 65 roubles, not far off the current rate, the price of oil should be $70, a recent Bank of America Merrill Lynch report found.

For ordinary Russians, it could be a tough year ahead. Those who were used to travelling abroad have already had to scale back as the rouble made the cost of visiting foreign cities prohibitive; and rising food prices have made it harder to balance the books for many families.

The 2016 budget, fixed in October, requires oil to be at $50 in order to run a 3% deficit within “acceptable” rouble rate limits, meaning if the price does not rise soon, cuts will need to be made or reserves spent. The war in Syria is an extra cost, and the announced increases in military spending are not likely to be reversed.

Venezuela

A mural depicts President Nicolás Maduro, who, having lost the Venezuelan National Assembly, has a battle to keep economy and his leadership afloat. Photograph: Luis Robayo/AFP/Getty Images

In most of the world, falling oil prices have caused significant reductions in petrol prices. But in the country with the world’s largest oil reserves, the oil glut could force a price rise.

“It’s probably the only place in the world where with oil prices so low, they may raise gasoline prices,” says Pedro Méndez, an informal taxi driver in Caracas, the Venezuelan capital, who fills the tank of his Ford Laser for less than a dollar.

But the lower the price of oil goes, the deeper Venezuela’s economy sinks. It’s near total dependence on crude exports for hard currency has seen the government of president Nicolás Maduro struggling to try keep the economy afloat.

The political effect is already being felt. Gripped by spiraling inflation, chronic shortages of basic goods and a quickly depreciating currency, Venezuelan voters this month gave the opposition an overwhelming majority in the new legislature, which takes office in January.

Each $1 drop in oil prices results in more than $685m in lost yearly oil income for PDVSA, the state-owned oil company, according to analysts.

And every drop in crude prices means less funding for the health, education and housing and other social welfare programmes that won Maduro’s predecessor, Hugo Chávez, widespread support for his self-styled “Bolivarian revolution”.

While dwindling oil revenue hurts the social programmes, Antonio Azpurua, a financial consultant with CFS Partners/LA Group, says it could be a blessing in disguise, allowing Venezuela to wean itself of its dependence on crude. “Venezuela needs to take advantage of low oil prices to build its industrial base,” he says.

With a super-majority in the National Assembly, the opposition could reverse some of Maduro’s populist measures, which have contributed to the current economic crisis. They could also choose to raise petrol prices.

Iran

Iran is rushing to implement the landmark nuclear accord in order to cash in on sanctions relief as early as next month, but the plummeting price of oil is tempering its expectations

Although the EU lifted Iranian sanctions in October after the Vienna nuclear agreement, the measures will only come into effect after what has become known as “implementation day”, the unknown date when the UN nuclear watchdog, IAEA, will verify that Iran has taken the necessary steps as outlined under the nuclear deal. Iran is expediting whatever it can to bring this date forward to as early as January.

In an effort to woo foreign investment in the post-sanctions era, Iran put a set of new lucrative oil and gas contracts, worth more than $30bn, on the market this month. But all these efforts have come at a time when global oil prices are falling as a result of a crude surplus of 2m barrels a day, a phenomenon Tehran blames on the Saudis.

“The drop in oil prices hurts all oil producers, not just Iran,” said Amir Handjani, president of PG International commodities trading services and a member of the board directors of RAK Petroleum.

“Saudi Arabia is very aware that Iran will be able to sell its crude unencumbered by sanctions on the international market very soon and will use all means at its disposal to make sure Iran doesn’t recapture the market share it lost over the past four years,” he said.

“Basically, Riyadh’s message to Tehran is simple: we can endure low oil prices for a while; can you?”

Iran’s economy faced huge economic problems in recent years due to international sanctions imposed over Tehran’s nuclear program. Plummeting oil prices only added to economic woes in a country with the world’s fourth-largest oil reserves.

The deputy managing director of the national Iranian oil company (NIOC) told the Guardian in September that the Iranian government was earning more from tax than oil for the first time in almost half a century as the country shifts its traditional reliance on crude to taxation revenues in the face of falling oil prices. Critics say Iran is unlikely to maintain that equation when the lifting of sanctions allows it to export more oil.

According to Opec, Iran on average was selling oil at $38.92 a barrel in November, $5.63 less than the average in October, which is the worst drop among the group’s members.